6.3 million Californians lack access to workplace retirement plan, Labor Center research finds

After more than a decade of declining private sector pension coverage, 6.3 million Californians do not have access to an employer-sponsored retirement plan, according to a new study released today (Thursday, June 7) by the University of California, Berkeley’s Center for Labor Research and Education.

“Recent household surveys indicate that the bottom half of California workers are not being served by the existing system of workplace retirement plans,” said Nari Rhee, a researcher at the center and author of the pension report.

“This is a serious problem,” she said, “because employer-sponsored plans are the most important vehicle for building retirement income after Social Security, and Social Security alone is not enough to get by on.”

“Without significant policy intervention to improve the retirement income security of private sector workers, California will face a serious elder poverty crisis in the coming decades,” Rhee wrote in the brief. “This will not only put retirees in serious hardship and increase financial demands on their families, it will also increase the need for subsidies and publicly-funded services, exerting strain on the state budget.”

In addition to calculating access to retirement plans by California’s private sector workers, Rhee also explored potential policy solutions, such as pooled accounts.

A program along those lines has been proposed in Senate Bill 1234. The legislation would create the California Secure Choice Retirement Savings Trust, a publicly sponsored, professionally managed retirement plan designed to close the private sector pension gap. The bill passed in the Senate last week and faces Assembly review. Meanwhile, Massachusetts, Connecticut and New York City are also considering policies to expand private sector pension access.

Rhee noted that the long-term decline in retirement plan access is attributed to private employers trying to reduce labor costs and financial risk by cutting back on defined-benefit pensions, funded entirely by employers, and recession cutbacks in defined-contribution plans like 401(k)s, which include employer and employee contributions.

The study sample covered the time period 2008 to 2010. It included wage and salary workers and self-employed workers whose businesses are incorporated. The number of workers without access to a retirement plan increases from 6.3 million to 7.9 million when self-employed workers whose businesses are not incorporated are included, Rhee said.

The main findings of Rhee’s research, based on data from the U.S. Bureau of Labor Statistics Current Population Survey, include:

- Workplace retirement plan access in California’s private sector declined steadily from 50 percent of workers in 1998-2000 to only 45 percent in 2008-2010.

- Some 6.3 million private sector workers ages 25-64 in California – 80 percent of whom work full time – have an employer who does not offer a retirement plan.

•Half of these workers earn less than about $26,000 a year, and 75 percent make less than about $46,000 a year.

•Over two-thirds of these workers are in small businesses with fewer than 100 employees, although 18 percent work in firms with over 1,000 employees.

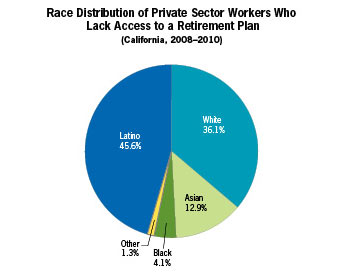

•Some 68 percent of these workers are people of color. Latinos make up 46 percent of the total, likely because they often are concentrated in low-wage jobs such as accommodations, food services, building services and residential construction.

- The typical California private sector worker who lacks access to a workplace retirement plan will receive Social Security benefits equal to just 50 to 60 percent of the amount needed to pay for basic expenses like food, housing and health care.

- A publicly sponsored retirement plan could improve retirement income security for low- and middle-wage private sector workers who lack access a workplace plan.

“For most people, retirement security is not about living in luxury, nor is it about just surviving; it is about having adequate resources to enjoy their families and interests after a lifetime of hard work while they are still in good enough health to do so,” Rhee concluded, calling an adequate retirement “part of the American Dream.”